iZUMi Research: the State of DEX and the future of decentralized trading

In this report, we analyzed the data of the largest liquidity pool WETH-USDC 0.05% on the top DEX — Uniswap V3, from both the taker side and maker side, as a representative to study the overall state of the DEXes under various market conditions. Meanwhile, we’ve done research on 20+ DEX products and DEX aggregators distributed in various ecosystems in the industry. Based on their operation and their recently announced development plans, we hope to take a glimpse at the possible trend of DEX in the medium term.

November 8 of 2022 will be another memorable day in the history of the Crypto industry. Within three days, FTX, the well-looking giant exchange collapsed, faster than anyone could have expected. The whole industry got disappointed and confidence has been hurt again: users once trusted those big exchanges, but in reality, exchanges failed them, again.

In the aftermath of FTX’s collapse, almost every exchange is trying to clear its name. Binance, OKX, Bybit, Bitget, Huobi and Gate.io have come up with their own solution for proof-of-assets, but in reality the scheme still needs to be audited by the relevant authorities (like auditing firms) and is not guaranteed to be completely safe. The greed of human nature is such that for the sake of “capital efficiency”, earning yields and amplifying their own risks are actually common in traditional finance. Everyone wants to make money when the market condition is good and stable, and everyone has a strong belief that they can put the risks under control and exit safely. But when the liquidity drains, the tide goes out and no one has time to put on their clothes.

Market was hit hard again, but from another perspective, this may be a new turning point for the industry.

Looking back, two years have passed since DeFi Summer, and during this time of industry cooling, various DeFi protocols have slowly faded from the public’s eyes.

The Economist’s cover article in 2015 called blockchain “the trust machine”, and this feature of blockchain technology has never changed over the past seven years. The emergence of DeFi, on top of the unique characteristics of the protocol of the blockchain, is a reversal against the blackbox of traditional financial institutions, proposing non-custodial, secure, transparent on-chain financial services, including lending, yield tools and all kinds of trading behaviors.

When we can’t trust humanity, it’s time to find the authentic “trust”.

As the underlying application layer on the blockchain, DEXes (Decentralized Exchanges) have become an infrastructure of almost every blockchain. Each public chain has its own DEX platforms, which often occupy a large part of the TVL and on-chain activities.

At the ecosystem level, most blockchains also support their own ecological DEXes. Meanwhile, the operational team of these DEXes will customize the features of their products to match the features of the blockchains they are on, as well as their own abilities and their judgments about the future. It’s important to know what their states and their plans are for the future.

In this report, we analyzed the data of the largest liquidity pool WETH-USDC 0.05% on the top DEX — Uniswap V3, from both the taker side and maker side, as a representative to study the overall state of the DEXes under various market conditions. Meanwhile, we’ve done research on 20+ DEX products and DEX aggregators distributed in various ecosystems in the industry. Based on their operation and their recently announced development plans, we hope to take a glimpse at the possible trend of DEX in the medium term.

Part 1: Observation from data side: a deep dive into the state of Uniswap V3

The earliest DEXes in 2017–18 mimicked the traditional order book model. Some of them include EtherDelta and DDEX. They struggled to have a healthy market depth and trading experience, due to the high cost of on-chain transactions. Even with the current high-performance infrastructure, the overall experience of order book-based DEX is still difficult to compete against CEX.

In late 2018, Uniswap implemented the Automated Market Maker (AMM) mechanism and released Uniswap V1.(Actually the idea is from Vitalik but Hayden Adams from Uniswap made it happen). The AMM mechanism is more like a vending machine on the blockchain, with a passive liquidity provisioning strategy adapted to the blockchain environment. The AMM mechanism combined with liquidity mining led to the explosion of on-chain finances, known as the DeFi Summer in 2020.

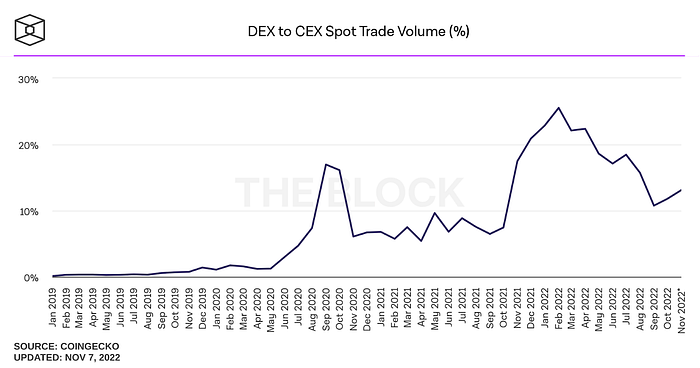

According to The Block, the overall trading volume across DEXes once accounted for 25% of total trading volume in the crypto industry and currently it remains around 15%.

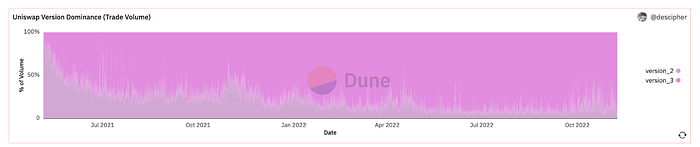

With the introduction of Uniswap V3’s concentrated liquidity AMM mechanism in March 2021 (where liquidity providers can provide liquidity in a customized price range instead of deploying liquidity into full range from zero to infinity by default), capital efficiency has increased by tens of times compared to the previous version. As we can see from the chart below, Uniswap V3 has started to bite up V2’s market share since its launch and now accounts for over 70% on average in terms of trading volume.

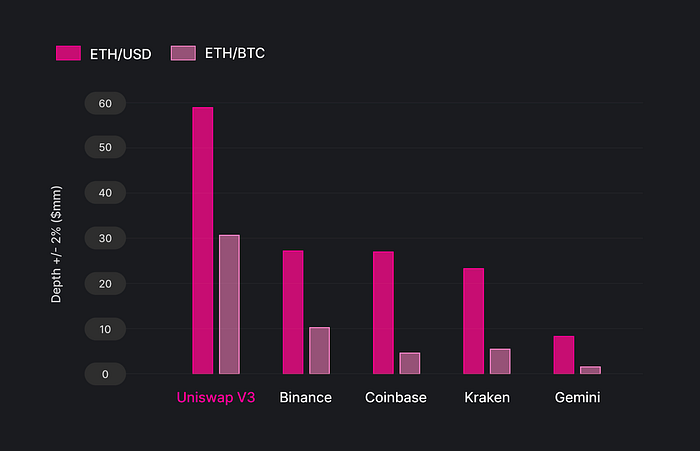

According to Uniswap’s research report in May, as the largest DEX, Uniswap once outperformed top CEXs such as Binance in terms of the market depth of major token trading pairs, with +/-2% of market depth of ETH/USD pairs on Uniswap reaching twice that of Binance in the timeframe of June 2021 to March 2022.

And now we’ve been through a deep bear market for the past year. What’s the state of Uniswap right now? We did a deep research, and will present it in the following part.

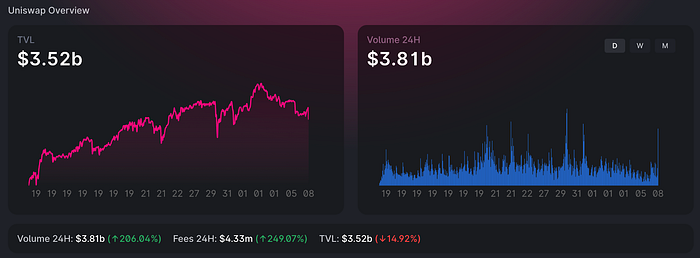

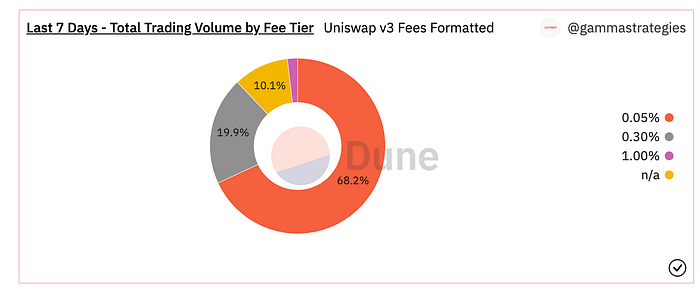

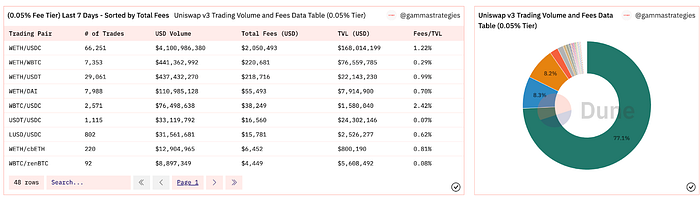

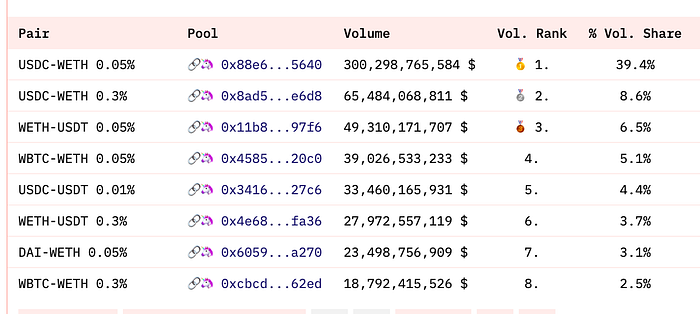

In the past 7 days (From Nov 2nd to Nov 9th), Uniswap V3 had a total trading volume of $7.8B, and the top 15 liquidity pools accounted for 89% of that, which is $6.95B. In terms of trading fee income for liquidity providers, the total trading fee for the past 7 days was $8.97M, with the top 15 pools accounting for $6.28M or 71%. The reason for this is that the top pools compete for trading volume and some liquidity providers choose to provide liquidity in pools that charge a lower percentage of trading fees, such as WETH/USDC where a large amount of liquidity is in the 0.05% fee tier pools. The long-tail tokens’ pools, on the other hand, mostly use a 0.3% fee tier or even 1% fee tier, so the volume is relatively small but the revenue share is even larger compared to the volume share.

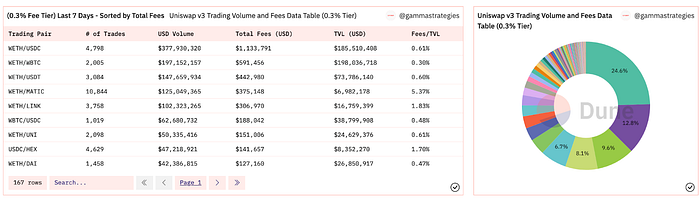

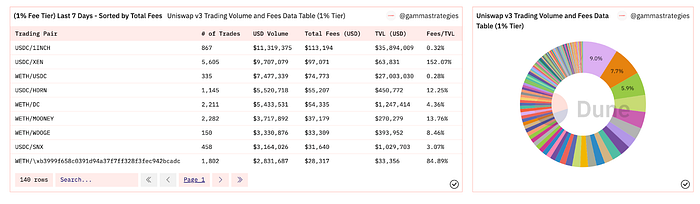

Since transactions on Uniswap will be routed to the lowest fee rate and best execution price, most transactions are concentrated in the 0.05% rate tier, which has good liquidity for major token pairs. Most of these liquidity are from the WETH/USDC 0.05% pool. Of the four rate tiers available, the 0.01% rate tier is relatively unique in that it is DAI’s official pool and is laid into Arrakis Finance to provide liquidity incentives. The state of the other three rate tiers are as follows.

The first one is the 0.05% fee tier pool, and most of its volume comes from WETH/USDC 0.05%, which accounts for 77.1% of the total trading volume in this fee tier. Other trading pairs include those of major tokens, stablecoins pool and other pegged assets trading pool, such as WETH/cbETH pool.

The composition of 0.3% fee tier pools is relatively evenly distributed. It consists mainly of various major tokens, as well as some other top 50 cryptocurrency trading pairs such as $MATIC, $LINK, and $UNI.

Overall, LPs of major asset pools are competing on the fee side, moving from 0.3% to 0.05% fee tier to compete for volume, trying to exchange fee for volume. Long-tail assets are more likely to choose the 1% fee tier pools rather than to compete at lower tiers due to higher volatility and risks of the assets, which makes those LPs more costly.

Deeping dive into the biggest trading pool

We obtained historical data from Dune Analytics. On Ethereum, Uniswap V3’s WETH/USDC 0.05% and 0.3% pools have $300.3B and $65.48B trading volume respectively ever since the launch of Uniswap V3, and account for 39.4% and 8.6% of the total trading volume. In terms of trading fee, those two pools have a total historical fee of $150.1 M and $196.44 M respectively, accounting for 12.4% and 16.3% of the total historical fee income.

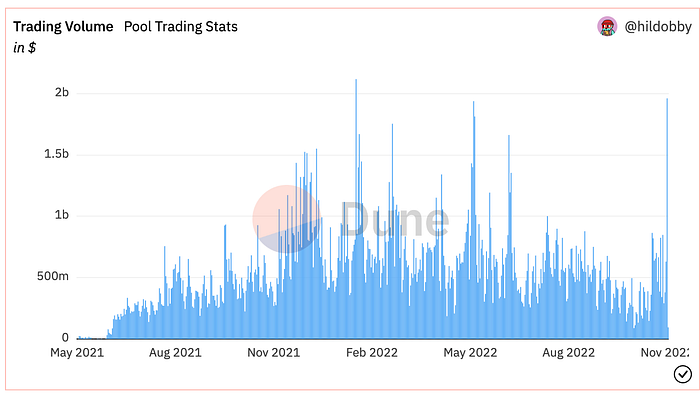

The following section takes a look at the Uniswap V3’s WETH/USDC 0.05% pool, which is the largest and most actively traded pool. Studying the current state of the main pool will give us a general idea of the current state of Uniswap V3 as a whole. Some facts are listed below, the first one is the daily trading volume:

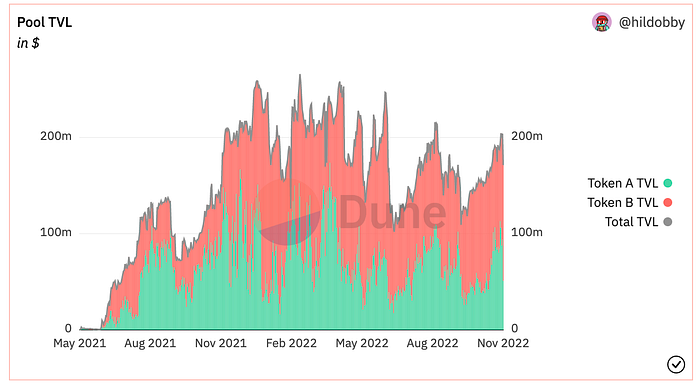

The pool TVL data is shown below. With the recent CEXes issues, DEXes such as Uniswap, as an on-chain infrastructure of the protocol layer, have been trusted by all users. The top DEXes will continue to maintain a stable trading volume. With the volume it comes with the fees to support the TVL and liquidity, and support the whole ecosystem. Overall the TVL of Uniswap V3 WETH/USDC 0.05% is relatively stable considering the fluctuation of ETH price, and is a highly liquid trading scenario.

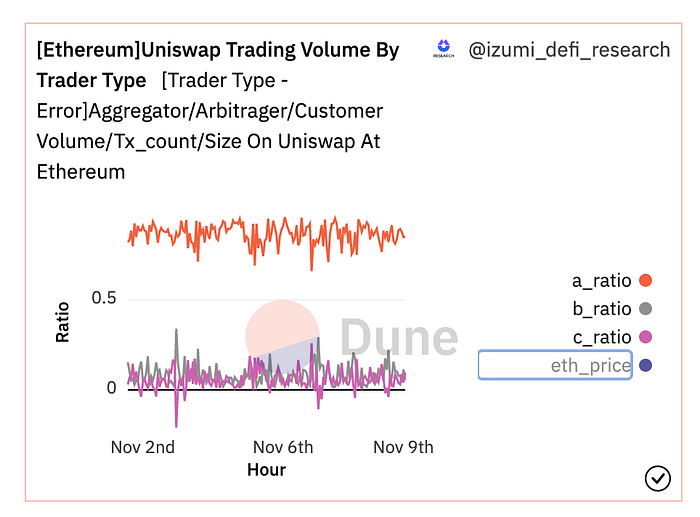

The on-chain data enables the distinction between bot addresses and real user addresses. Due to the nature of on-chain trading, price discovery generally occurs on major CEXes, and then the DEXes price is leveled out through arbitrage between the various bots. There will also be various types of trading bots on-chain. And the percentage of real users is an important indicator of how active on-chain trading is. In the current market, the Uniswap V3’s WETH/USDC 0.05% pool has a bot trading share of over 85%.

We can consider that this data is highly correlated with market sentiment. Below is the same kind of data from 360 days ago, while the market was still bullish, and the percentage of bot trading volume is maintained at around 60%.

As you can see this data does correlate with the market, in a bear market environment, the overall trading volume declined, along with a significant decline in the percentage of real users on-chain.

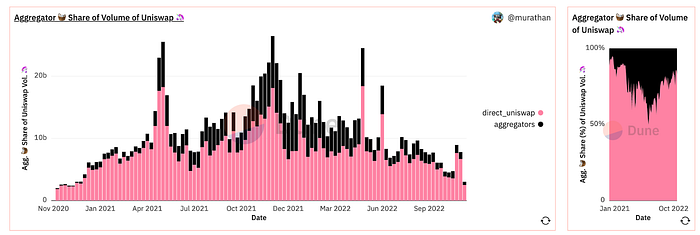

Another perspective to think from the trader’s side is to look at DEX aggregators. In traditional finance, there’s also a two-layer structure: exchanges and brokerages. Normally users will not trade in exchanges such as NASDAQ, instead they will register accounts at brokers such as Robinhood. Here DEXes like Uniswap are the NASDAQs, and aggregators are the brokers.

The share of aggregators increases significantly in a bullish market environment and then decreases. The main reason for this is that during bear markets, on-chain activities shrink, and most of the trading volume comes from arbitrageurs and other trading bots, which interact directly with the Uniswap pool and generally operate less through aggregators.

From the Taker’s side, the overall on-chain situation is relatively pessimistic. During the bear market, the number of real users on-chain plummeted while the overall trading volume and TVL shrank, and the major trading volume returned to the top platforms. From the perspective of token trading pairs, mainstream token trading ratio (trading shares) rebounded, while long-tail assets were in the “freezing period”.

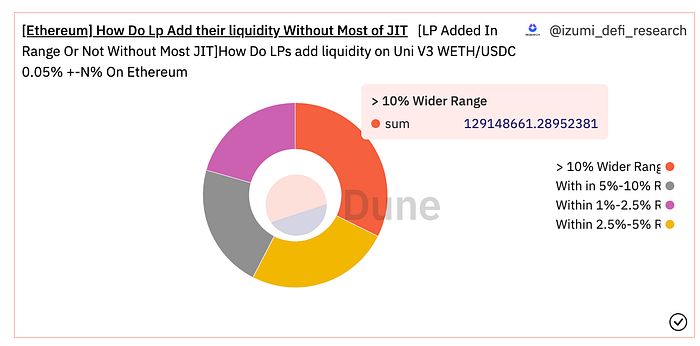

From the Maker’s side, in Uniswap V3 WETH/USDC 0.05% pool, liquidity providers will choose to provide liquidity within 10% of the price range to earn more trading fees, making their liquidity more capital efficient.

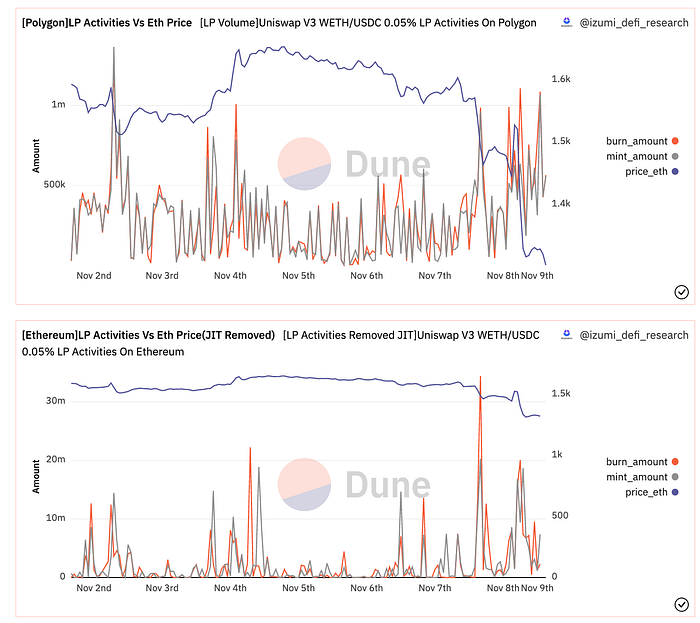

Meanwhile, the pool’s liquidity providers have relatively fewer adjustments when compared with other blockchains. We compare the LP activity of Polygon (above) and Ethereum (below) in the chart below, and it is clear that adjustments are more frequent on Polygon, while on Ethereum there’s more big adjustments but the frequency is low.

The chart above shows LP activities in the Uniswap V3 WETH/USDC 0.05% pool on Polygon, with Mint and Burn being the number of dollars added and withdrawn from LPs, respectively. And put together with the dark blue Ether price curve, LPs on Ethereum are less sensitive to price fluctuations than liquidity providers on Polygon, as LPs on Ethereum are mostly using large amounts of money and this makes sense as adjustment on Ethereum is slow and costly.

Overall, in a bear market, trading volume and active users on Uniswap v3 declined, but liquidity providers remained active and Uniswap maintained good liquidity. And overall trading liquidity is actually better due to factors such as JIT liquidity (short-term liquidity that supports large order transactions).

However, in terms of general user experience, Uniswap V3 still has too much room for improvement, with issues such as MEV attacks, slippages, uncertainty in trade execution results, and user experience issues such as lack of support for limit orders, wallet management complexity, and gas fees. This part of the problem will not necessarily be solved by the DEXes. Traditional financial markets also have a two-layer structure: users do not go directly to NASDAQ to trade, but trade through brokers, which are the distribution channels.

Here, as mentioned earlier, DEXes is much like exchange such as NASDAQ, and the aggregator is the broker, which is the channel to solve the user experience problem. In the second half, we tracked the current status and future plans of the top 20 DEXes and aggregators to examine DEX development trends.

What will the future be? These 20 DEXes/aggregators might give us the answer

In the first half we looked at the top one DEX — Uniswap V3 on Ethereum — from the data side, which represents only a fraction of the DEX’s present and past. In order to see the future direction of DEX evolution, we have compiled a list of 20 DEXes that have recently evolved on the product side and market side, and from their product design and narrative, we can see the following trends.

The emergence of CL-AMM DEXes on multi-chain, and the professionalization of AMM market making

Recently we have seen a number of concentrated liquidity DEX products(which is similar to Uniswap V3 but still there’s lots of differences) launched on other ecosystems, some of them are:

- Ref Finance V2 of Near ecosystem, the AMM model design is technically supported by iZUMi Finance

- Arctic of Aurora ecosystem, the DEX design is supported by iZUMi Finance

- Trader Joe V2, on Avalanche ecosystem. Its new AMM design refers to iZUMi’s DL-AMM design.

- Duality of Cosmos ecosystem, which is a DEX with concentrated liquidity and limit order function

- Quickswap V3 upgrade to concentrate liquidity AMM model, with flexible fee adjustment function

- Sui ecosystem’s MoveX is also a DEX with concentrated liquidity and limit order function

Some of those examples are upgraded from old V2 style (which users need to provide liquidity in price range from zero to infinity by default) to some kind of concentrated liquidity model (allowing liquidity providers to offer liquidity within a customized price range to improve capital efficiency). Others are newly designed DEX on new ecosystems.

There are also technology providers to help DEX upgrade, such as Algebra which provides the underlying technology and license to help Quickswap upgrade to its V3.

Take one more look from the Maker’s perspective. According to discussions from Friktion Labs and Uniswap Labs on crypto

Twitter: https://twitter.com/thiccythot_/status/1589022227437039616

and our own research over Uniswap V3’s LP: Why shouldn’t you be the liquidity providers on Uniswap V3 for now? | by iZUMi Finance | Medium

Although DEX’s permissionlessness and open nature allow the general public to participate in liquidity provision, which is traditionally reserved for professional market makers with certain licenses, and liquidity mining is a new way to distribute token. In reality, most liquidity providers lose money overall, even with Uniswap V3.

Plus, the emergence of Uniswap V3’s concentrated liquidity model makes liquidity provision more complicated, and complicated things need professionalization.

With the recent proliferation of DEXes with centralized liquidity designs in multiple blockchain ecosystems, we can expect more market-making teams focused on providing professional liquidity services for other projects in centralized liquidity DEXes in the future, considering the special on-chain environment (including transaction confirmation latency, MEV, fee mechanism, slippages, etc.), and the completely different mathematical calculations and characteristics of AMM model and traditional Order Book.

At present, the main professional market making is concentrated in major and most traded tokens. Long-tail tokens are generally still using V2 style’s full price range liquidity combined with liquidity mining in view of the complexity of adjusting positions and the difficulty of distributing token incentives for concentrated liquidity providers. In the future, considering the high capital efficiency of concentrated liquidity, combined with the demand for on-chain native trading activities (such as GameFi, which naturally requires on-chain trading scenarios), concentrated liquidity provision service solutions around long-tail tokens will gradually mature. iZUMi Finance has positioned itself as an on-chain liquidity service platform from the beginning, and launched LiquidBox, an liquidity mining scheme for concentrated liquidity, with multiple strategies to allow projects to achieve better on-chain liquidity with less intervention and lower costs.

Focusing on capturing traffic, user experience upgrade

The top DEXes are focusing on bringing in new users, including improving user experience and achieving traffic exposure on both the mobile and the web end. Uniswap, after acquiring Genie, the NFT aggregation marketplace, has integrated Sudoswap to upgrade the web-side APP and included NFT trading as well, thus it can capture users from both sides. DODO, on the other hand, is pushing mass adoption and promoting it on Web3 and traditional traffic portals, implementing gasless transactions and limit orders to capture more users. In addition, Sushiswap implements a gasless limit order function. Chainge, the cross-chain wallet, is mainly promoted on the mobile app.

Uniswap, Pancakeswap, and others have recently launched price charts to free users from the hassle of using additional chart tools. iZUMi Finance will soon launch iZiSwap Pro, featuring its compatibility with limit order and AMM, to achieve a better user experience comparable with major CEXes.

On the maker’s side, some V2 style DEXes offer Zap functionality for users to add liquidity with just one transaction. In addition, a team coached by iZUMi won third place in EthGlobal hackathon for implementing Uniswap V3’s one-click liquidity adding solution. iZUMi Finance also provides one-stop liquidity services to project owners through its V3 liquidity mining tool LiquidBox and accompanying market-making strategy.

hybrid AMM (Automated Market Maker) + RFQ (Request For Quote) + LOB (Limit Order Book)

AMM is truly an innovation, while it is adapted to the complex environment on-chain, it also brings many other problems, such as uncertain transaction execution results, slippages, and is easy to be exposed in various forms of attacks such as MEV, etc. Just thinking about MEV, in order to reduce the impact of it, there are many solutions and attempts from the network level to the protocol level, but it is difficult to be thorough.

Limit orders can avoid these problems of AMM, with aggregators/DEXes such as 1inch, DoDo, Sushiswap introducing limit order functionality, as well as Pancakeswap implementing limit order functionality through Gelato, and iZUMi Finance’s iZiSwap designing DL-AMM to be compatible with AMM and limit orders.

However, traditional limit orders suffer from the problem of front-running attack, and most aggregators currently use centralized limit order solutions that still suffer from such problems. iZUMi’s DL-AMM is the best solution right now as it directly implements the on-chain order book and does not have a significant increase in gas overhead compared to a typical AMM.

In addition, Binance’s newly launchpool project Hashflow, 0x’s Matcha, and many other projects in the primary market all adopt RFQ mechanism, in which users propose a demands, and the platform provides quotes for users off-chain through an oracle or market maker, and then implements atomic swap on-chain, which does not have problems such as slippages and brings certainty to transactions. However, such a mechanism cannot achieve price discovery, and the price discovery mechanism is entirely dependent on price input from the oracle. GMX can also be considered as a RFQ mechanism based DEX.

DEX-based on-chain financial products, packaging liquidity for sale

This trend was also mentioned by our research team in the previous DeFi On-Chain Funds section (https://izumiresearch.substack.com/p/defi-on-chain-fund). In the case at the time, Umami Finance came with a USDC vault that generated revenue through GMX’s GLP, and hedged its exposure to the volatile asset portion of the GLP through Mycelium (formerly Tracer DAO) to provide users with an annualized 20% return. The product was eventually closed due to Mycelium’s poor performance in times of high price volatility.

The concentrated liquidity LP tokens represented by Uniswap V3 is a very flexible asset class that can be used to simulate the payoff of other derivatives. For example, setting liquidity in the price range below the current price and then holding a spot of equal value allows for the simulation of call options within a certain price range.

Plus, the traditional CEX dual currency financial products offered with low-buy and high-sell strategies are also essentially using a certain market-making strategy to provide returns to users. DEX’s LP token is fully capable of achieving the same product and providing the same level of yield. These products are essentially a win-win strategy for users. For them, they buy strategies and earn yield. For DEXes, users add more liquidity to the platform via the strategies.

iZUMi Finance is experimenting in this area and will launch related financial products soon.

What will be in the future?

This is an issue we continue to think about. The DEX protocol itself, as the underlying infrastructure, has great features such as openness and permissionlessness. Those features allow a series of other ecosystem products to emerge based on the DEX protocol.

As mentioned in the trends in this section, the two-layer architecture of aggregator + DEX realizes the distribution channel of traffic and liquidity. At the same time, the front-end experience is CEX-ized and the back-end realizes professional one-stop liquidity provision services and supporting financial derivatives. In this supply chain, there will be many opportunities inside, either in the form of products or services.

With any centralized entity, there is always the risk of a single point of evil. As Arthur Hayes, founder of BitMex, mentions in his latest article Speechless:

“Centralized exchanges will always face these issues of mistrust on behalf of their customers. FTX was not the first high-profile exchange to fail and it won’t be the last.”

The asset transparency, security, and non-custody offered by DEX, combined with its open nature, will prove itself reliable as centralized institutions continue to rise and fall.