Understanding $DAI — Don’t Let It Be Wrapped $USDC Anymore

We all know MakerDAO & $DAI stablecoin. People overcollateralize their crypto assets and borrow from MakerDAO in $DAI-denominated loans. However, since the PSM module introduced in late 2020, $DAI increasingly looks like a wrapped $USDC. Today, we take you to review MakerDAO from a balance sheet perspective and get to understand the underlying reason for its recent move: investing in U.S. treasuries. I believe you will find this is an extremely interesting step and could bring a far-reaching impact on DeFi.

Over-Collateralized Crypto Loan and Stablecoin $DAI

MakerDAO offers two products: crypto loans & a stablecoin $DAI.

Just like AAVE and Compound, MakerDAO is a DeFi lending protocol. Borrowers deposit eligible crypto collateral such as $ETH, and the protocol will issue a $DAI denominated loan. MakerDAO offers various vaults with different collateralization ratios and borrowing interest rates. In the below example, a high collateralization ratio of 170% for $ETH corresponds to a lower interest rate at 0.5%, and vice versa.

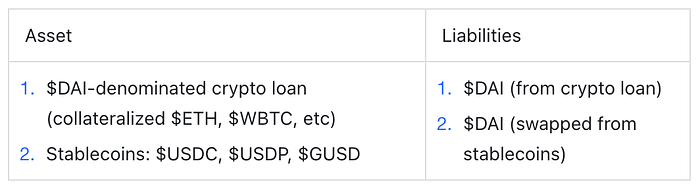

This is the most basic format for MakerDAO. The balance sheet for the protocol at this stage is straightforward.

The loans are assets of MakerDAO as they generate interest revenue, and $DAI is the liability to the protocol.

For a fiat-backed stablecoin like $USDC, the balance sheet looks like as below. Users gives Circle — the $USDC issuer their USD, and in return, Circle issues a contractual IOU, which is the $USDC.

Circle promises to always redeem 1 $USDC for 1 dollar. The key difference here is there is no contractual obligation for MakerDAO to exchange 1 $DAI for $1 dollar. $DAI is backed by crypto over-collateralized loans and is pegged to $1 dollar. The peg is maintained by sound risk management practice (e.g. setting sufficient collateralization level) and a robust liquidation mechanism such that to avoid a rapid decline of collateral value and failure to liquidate. In that case, the asset (crypto-collateralized loan) will be less than the liability (issued $DAI), and the protocol is insolvent.

Peg Stability Module

MakerDAO introduced the Peg Stability Module (PSM) in 2020 during a time of huge market volatility. It allows users to costlessly swap between stablecoins ($USDC, $USDP, $GUSD) and $DAI.

The PSM strengthened $DAI peg through arbitrage as now traders are able to arbitrage the price difference between $DAI and other fiat-backed stablecoin.

Unlike the overcollateralized borrowing vaults such as $ETH vault, users of PSM don’t retain ownership of the asset, instead, they swap the asset directly for $DAI. $DAI can also be swapped back into PSM module and with stablecoins returning back, up to the amount in PSM module.

The MakerDAO’s balance sheet after introducing PSM.

On the asset side, stablecoin assets are added in addition to the $DAI-denominated crypto loan. On the liability side, the Maker protocol accrue a $DAI debt which is backed by the stablecoin asset users trade into the PSM in exchange for $DAI.

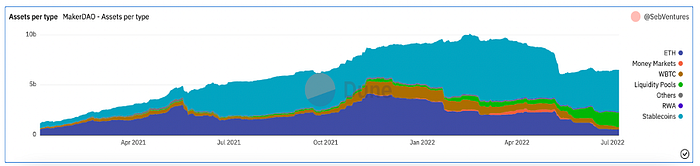

Because the price for swapping between stablecoins and $DAI using PSM is set at 1, this enables risk-free arbitrage opportunity when the $DAI price deviates from $1. PSM has attracted huge money inflow since it was introduced in late 2020. The share of stablecoins backing $DAI has since continued increasing.

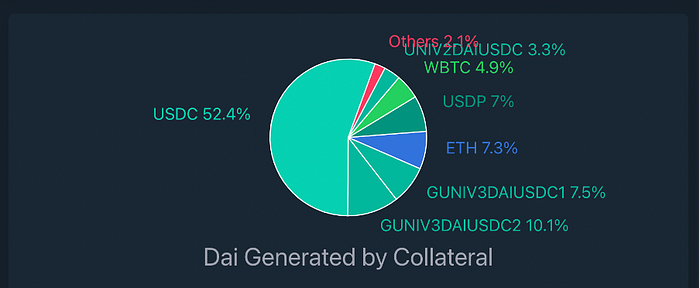

Currently, the majority of $DAI is generated by PSM, mainly 1:1 backed by $USDC, which accounts for more than 50% of the total $DAI supply.

On the positive side, a centralized fiat stablecoin helps $DAI maintain a stable peg to the US dollar. However, such a large percentage of the assets backing $DAI are centralized stablecoins also pose significant problems and risks.

First, it makes MakerDAO fundamentally distant from the lending business. MakerDAO is supposed to be a lending protocol, earning interest from over-collateralized crypto loans. However, the two main collateralized crypto assets, $ETH and $WBTC, together represent less than 15% of the total reserve assets. Nearly 60% of the assets are derived from the stablecoins in the PSM module, which do not earn any revenue for the protocol.

$DAI has somehow become a Wrapped $USDC… (and has helped boost the demand of $USDC for free)

At the same time, the huge amount of fiat stablecoin reserve assets creates counterparty credit risk for MakerDAO, where these $DAIs are minted from stablecoins issued by centralized institutions as reserve assets. If these issuers fail to maintain their respective stablecoin pegs or exchange back their stablecoins with promised 1:1 ratio, they are effectively in default. Right now, the single exposure of $DAI to $USDC represents over 50% of the total supply of $DAI. This creates a single concentration of risk to the protocol from Circle, the issuer of the centralized stablecoin $USDC.

Investing in U.S. Treasuries

Reducing the exposure risk to $USDC and improving the profitability has been two main focuses for MakerDAO since last year. While assets that collateralized crypto loans are not touchable by Maker protocol as the protocol doesn’t own those collaterals, stabelcoins in PSM are owned by Maker protocol and can be reinvested into yield-generating assets.

The focus is to improve profitability and to reduce risk, so putting $USDC into DeFi yield-generating strategies is probably not a good idea. Considering $USDC is backed by dollar deposits and U.S. Treasuries, directly investing in U.S. Treasuries could reduce the exposure risk to Circle and essentially hold the same underlying asset.

While the protocol is not able to directly hold financial assets as there is not a legal entity representing the DAO. MakerDAO has designed a trust structure to indirectly hold real-world assets including treasuries. The detail of the trust structure is out of the topic of this article, for the interested party, you can find a detailed explanation in Maker’s governance forum.

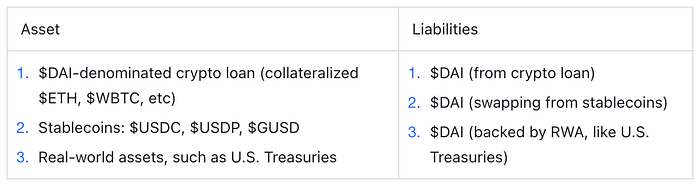

The resulting impact on MakerDAO’s balance sheet will be:

A Small Step with Huge Implication

Although it doesn’t attract too much attention in the industry, this is a significant step in DeFi.

Directly holding U.S. treasuries significantly reduce the counterparty risk. Holding $USDC incurs two levels of counterparty risk to MakerDAO. Firstly, the risk of $USDC’s issuer — Circle. Secondly, $USDC itself is backed by a combination of assets including dollar deposits in banks and U.S. treasuries. $USDC faces counterparty risk to those banks.

Furthermore, Circle doesn’t pass on the yield it earned from reserves (bank deposits & treasuries) to $USDC holders. All yield becomes Circle’s profit. By directly holding U.S. treasuries, the yield is earned by the Maker Protocol and accrues to the surplus buffer.

The most important implication is that $DAI could transform itself into somewhat a decentralized fiat-backed stablecoin.

At this stage of crypto development, it is clear that fiat-backed stablecoin like $USDC and $USDT are still the dominant medium for transactions. The era of stablecoin that could be detached from U.S. dollar assets probably has yet to come. However, centralized fiat-backed stablecoin issuers like Tether or Circle, have always the counterparty risk associated with them. You have to trust these companies to act in good faith, and trust their management would not engage in risky behavior for their own benefit.

MakerDAO is a decentralized organization governed by $MKR holders. All decisions have to be approved by the community including the asset allocation and what to do with the yield generated from the investment. In this way, $DAI enjoyed the stability advantage stemming from the U.S. Treasuries’ backing and at the same time avoiding the trust problem associated with a centralized entity.

Closing Thoughts

When people realize $DAI could become a decentralized fiat-backed stablecoin, I believe we will see an explosion of $DAI demand. And when people realize the yield generated from this investment will accrue to the protocol, I believe the market will reprice the governance token $MKR. Again, this seems to be a small step, but I believe this will bring a far-reaching impact to the crypto industry.

The original post can be found here at Tokeninsight.