Will Genesis Go Bankrupt? A Review of the Genesis/DCG Incident

The collapse of FTX triggered an avalanche in crypto. Rumors of insolvency spread among centralized exchanges, who rushed to show proof of reserve. Alameda’s trading partners raced to secure whatever assets that were not gambled away. Venture funds had no choice but to write off one of the worst investments in finance history. Genesis and Digital Currency Group (DCG) are the most notable names among those affected. FTX/Alameda borrowed billions from Genesis, which had already suffered significantly when Three Arrows Capital (3AC) went under. Speculators believe Genesis will have to file for bankruptcy if there’s no new funding to cover the losses. Genesis/DCG may sound unfamiliar to ordinary crypto enthusiasts because they primarily serve whales and institutions. In this article, we will first explain what Genesis/DCG is and then discuss what happened and what might happen next.

What is Genesis/DCG?

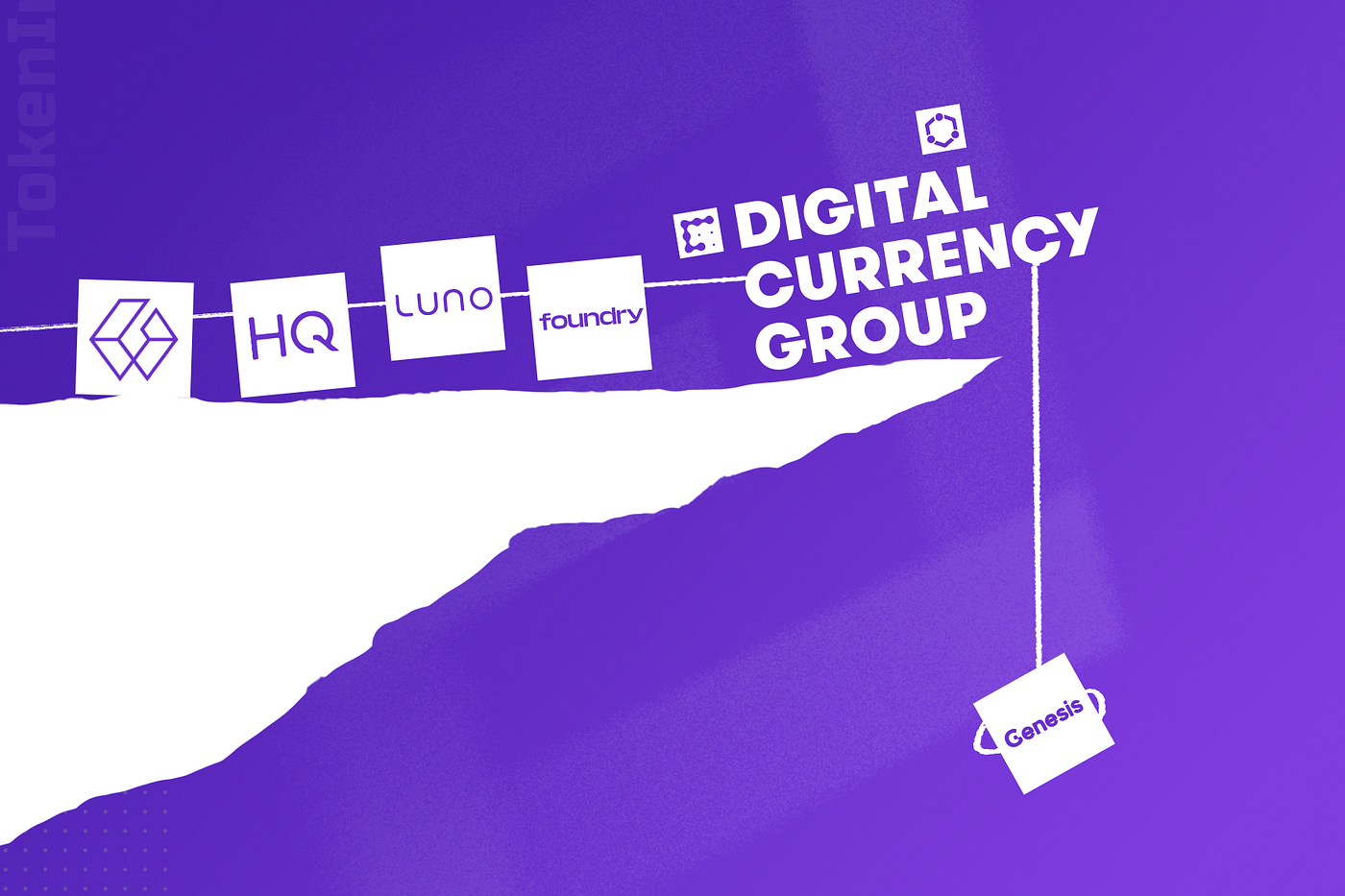

Digital Currency Group (DCG) is a venture capital company focusing on crypto. It was launched in 2015 by Barry Silbert, who previously founded and sold SecondMarket to Nasdaq. DCG has made 200+ venture investments and owns seven subsidiary companies: Genesis, Grayscale, CoinDesk, Foundry, Luno, TradeBlock, and HQ.

DCG started from Genesis. Genesis is an institutional digital asset financial services firm. It aims to combine market data, exchange connectivity, and liquidity to provide an all-in-one service to institutional investors.

It provides four services:

- Trading

With access to a network of trading partners, it offers market-making services and two-sided liquidity for buyers and sellers of digital assets with tailored execution.

- Lending

As a counterparty for institutions, Genesis facilitates two-way loan originations between lenders and borrowers. The minimum lending size is 100 units of BTC, 1,000 units of ETH, $2 million of USD, or $1 million of altcoins.

- Derivatives

Genesis offers customized derivatives solutions. It can trade vanilla options and forwards in bilateral OTC format or on-exchange listed format.

- Custody

Genesis offers institutional-grade security and infrastructure to manage, move and store digital assets, with a deposit minimum of $1 million in USD notional.

Grayscale is now the world’s largest digital currency asset manager, allowing institutions to gain exposure to crypto via vehicles such as the Grayscale Bitcoin Trust (ticker: GBTC).

CoinDesk is a news site specializing in cryptocurrency. It was founded by Shakil Khan in 2013 and acquired by DCG in 2016. The entire FTX/Alameda downfall started from a CoinDesk article questioning their balance sheet.

Foundry is a financing and advisory company providing miners and manufacturers with the resources needed to maintain and secure decentralized networks.

Luno is a crypto investment app that contains a digital asset exchange and a wallet.

TradeBlock is an institutional streamlining platform that enables institutions to automate their crypto asset trading workflows.

HQ is a wealth management platform for digital asset entrepreneurs and investors.

According to the official announcement, the trading arm of Genesis is the only business affected by recent events. Other subsidiaries are independent entities and remain fully operational.

Some speculate that DCG will be forced to sell bitcoin held by Grayscale’s GBTC to cover the losses of Genesis trading. This is nonsense. DCG does not own the bitcoins in GBTC. GBTC customers do. And the bitcoins are held in custody by Coinbase. DCG can sell Grayscale equity to generate cash, but DCG can’t sell the bitcoins directly.

What Happened to Genesis?

As the market learned FTX/Alameda was beyond saving, many began questioning whether their close business partners may be dragged along on the sinking ship. Genesis, one of the largest crypto trading firms, came under the spotlight.

Genesis pretended everything was all right initially, but things quickly lost control.

Genesis first claimed they had managed their lending book and had no material net credit exposure.

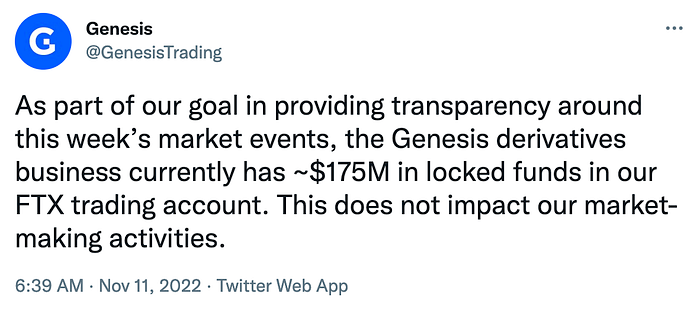

However, less than 24 hours later, Genesis provided an update, admitting that they had incurred a total loss of ~$7 million across all counterparties, including Alameda. Still, $7 million was no size for a behemoth like Genesis, which was moving billions daily.

Genesis finally dropped the bomb five days later when it suspended redemptions and new loan originations. Genesis conceded that the default of 3AC negatively impacted the liquidity and duration profiles of their lending entity Genesis Global Capital, while FTX created unprecedented market turmoil, resulting in abnormal withdrawal requests that exceeded their current liquidity.

They announced that they would be sourcing new liquidity to save the business. There were rumors that Genesis was looking to raise $1 billion. But similar to FTX, Genesis still needs to have a savior. They promised to deliver a plan for the lending business this week. It’s already Friday, but nothing has been released. The more time it takes, the worse news will likely come out.

However, one must note that Genesis’ spot and derivatives trading and custody businesses remain fully operational. Genesis Global Trading, the broker/dealer that holds the BitLicense, is independently capitalized and operated — and separate from all other Genesis entities. The troubling part is Genesis Global Capital.

New York Times reported on Nov 23 that Genesis Global Capital had hired the investment bank Moelis to explore options, including bankruptcy. On the same day, via a leaked letter to shareholders, Barry Silbert disclosed that DCG had a roughly $575 million liability to Genesis Global Capital.

What’s Next, Will Genesis Go Bankrupt?

Without immediate new funding, the most likely outcome for Genesis is that Genesis Global Capital, the lending arm, files for bankruptcy. It is still being determined whether other Genesis businesses and DCG can generally stay afloat.

SBF assured the crypto community that FTX.US operated independently and faced no financial trouble before FTX.US was included in FTX’s bankruptcy filing.

But the case around Genesis is more complicated. FTX.US was worthless since SBF moved customer deposits to Alameda. But many of DCG’s businesses still look like good acquisition candidates. However, it was reported that Genesis has $2.8 billion in outstanding loans on its balance sheet, with about 30% of its lending made to related parties, including its parent company DCG. The details are not available to the public, so any predictions are guesswork.

Ram Ahluwalia, CEO of Lumida Wealth, argued that Genesis is the only full-service prime broker in crypto and plays a critical role in enabling large institutions to access crypto and manage risk. However, because Genesis pioneers the prime broker sector in crypto, it cannot benefit from existing infrastructure, such as liquidity, standards, inter-dealer relationships, clearinghouses, and deposit financing, that traditional prime brokers enjoy.

This has two significant implications.

First, Genesis must seek to match the duration of its assets (its loans) with liabilities (its borrowings). A bank can borrow short-term (your deposit account) and lend for a longer term (a thirty-year mortgage). A bank-backed traditional prime broker can tolerate a mismatch in the duration of its assets and liabilities because it has FDIC insurance as the lender of last resort and a liquid market with standardized contracts. On the contrary, a non-bank prime broker like Genesis must seek to eliminate any mismatch in duration, which is not easy.

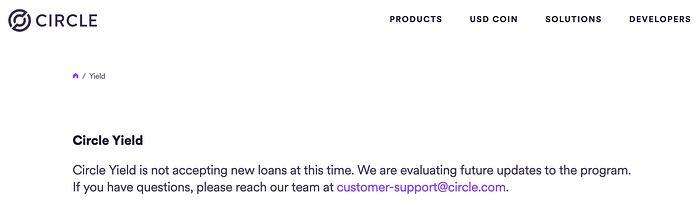

Genesis’ funding sources included borrowing via the Gemini Earn and Circle Yield programs. These are short-term sources of funding. If those funding sources dry up, then Genesis is forced to liquidate its loan book at unattractive prices.

Unfortunately, Circle has already shut down its Circle Yield service, which means Genesis’ funding source is decreasing.

n addition, longer-term loans are illiquid and may not be callable or redeemed at par. This exposes Genesis to a potential “bank run” that is already happening. If everyone withdraws deposits at the same time, Genesis can’t liquidate its assets fast enough due to contract obligations or lack of liquidity to meet those demands. Therefore it paused withdrawals last week.

Second, outside the lending business, Genesis is the buyer to every seller and seller to every buyer in trading and derivatives. Genesis has to seek to run a matched book at all times. As a result, Genesis takes on significant counterparty risk during its course of business. If their counterparty, e.g., 3AC, fails, then Genesis is in trouble.

The counterparty risk is exacerbated because there is no CeFi or DeFi clearinghouse to sell the risk to, and there is no inter-dealer market consisting of higher-quality participants.

A counterparty blow-up means Genesis has directional exposure and will incur a capital loss. This can cause a loss of confidence and lead to a bank run.

The prime broker business is an attractive fee machine if a robust ecosystem is in place to cover unexpected losses. But in crypto, due to its early-stage nature, it’s a fragile business prone to counterparty risk, bank runs, and asset-liability mismatch, which is exactly what happened to Genesis.

So, where does Genesis/DCG go from here?

There are two solutions.

The first and most obvious move is to raise equity at the parent company (DCG) level and inject fresh capital into the subsidiary (Genesis) to cover losses and restore confidence, a route taken as widely reported in the news.

But Genesis is capital intensive. It relies on capital and borrowings to make loans, but its funding sources have dried up. It desperately needs to find new cheap, yet reliable funding sources. Otherwise, Genesis cannot sustain its regular business. And the Fed’s raising rate only makes things worse.

The other move for Genesis is to get acquired by powerhouses from traditional finance. This will be challenging due to regulatory scrutiny, questions about asset quality, and the overall risk-off sentiment. But Genesis could continue to generate cash in the right hands.

Suppose no buyers in the market are interested in DCG or Genesis. In that case, as discussed earlier, the only possible outcome is the organized bankruptcy of Genesis Global Capital, the lending subsidiary of Genesis.

Closing Thoughts

The FTX collapse can be viewed as crypto’s Lehman Brothers moment, and it will cause broader contagion, industry consolidation, and more vigorous regulatory scrutiny. We will experience a prolonged period of financial and political uncertainty. However, the bright side is that good business will be cheap during this period. It is a good time to consolidate your crypto holdings into a few high-conviction bets, with sustainable business models experiencing increasing utility and adoption.